Car insurance has already become more expensive for many drivers, and tariffs can add even more pressure. When governments impose tariffs on imported vehicles, parts, steel, aluminum, or other key inputs, the costs do not stop at the factory or the dealership. They often ripple across the entire automotive ecosystem, including claims, repairs, replacement values, and ultimately auto insurance premiums.

For consumers, that matters because insurance pricing is closely tied to how much it costs to repair or replace a vehicle after a covered loss. If repair bills rise, insurers generally adjust rates to reflect that higher risk.

This guide explains how tariffs can affect car insurance, why repair and replacement costs matter so much in premium pricing, and what drivers can do to reduce the financial impact.

Why Car Insurance Costs Have Been Rising

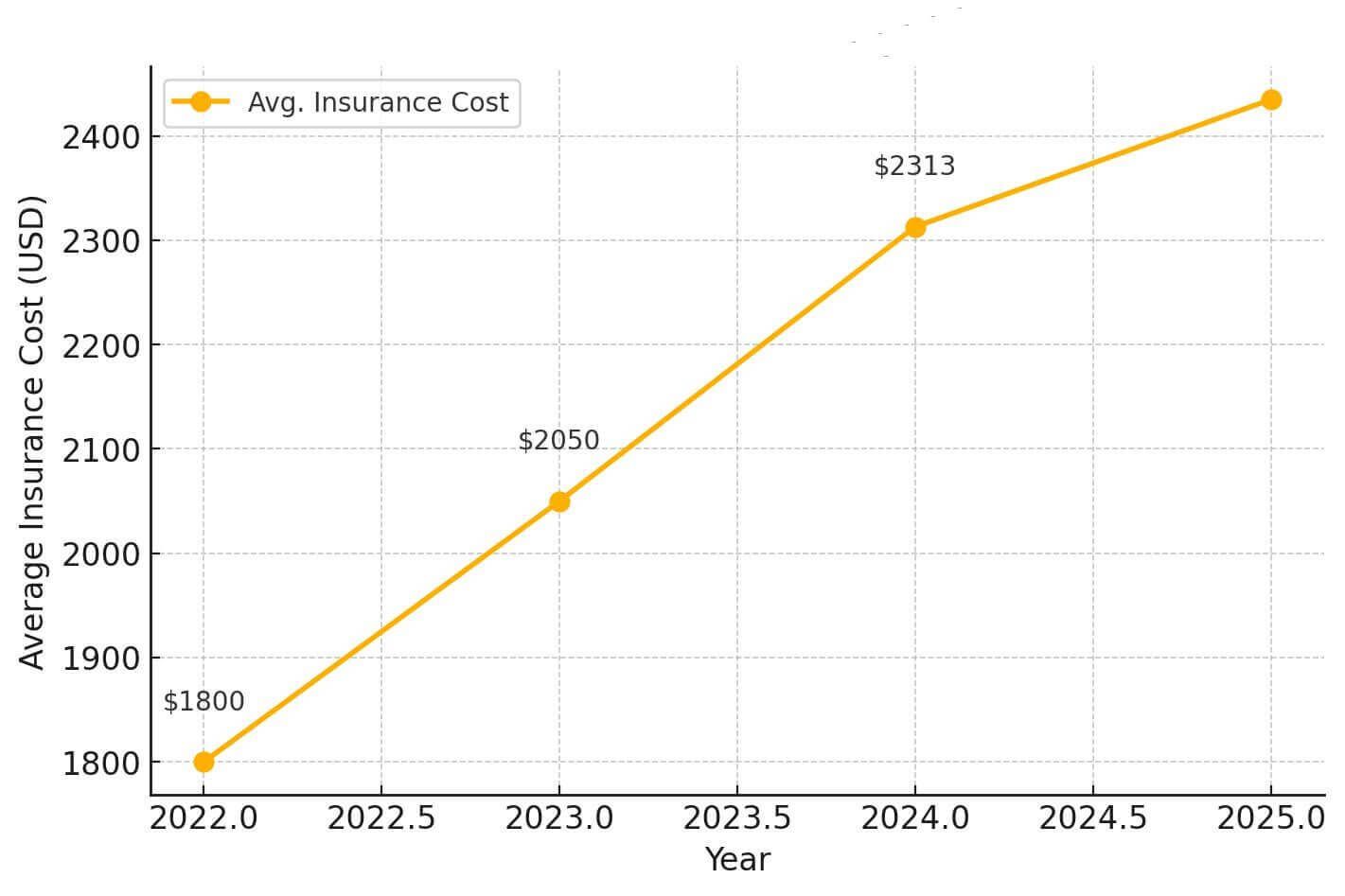

Auto insurance premiums have been under pressure for several years, driven by a mix of claim severity, expensive vehicle technology, climate-related losses, litigation trends, and inflation in vehicle repair and replacement costs.

The pressure has been visible in government inflation data as well. U.S. Bureau of Labor Statistics data showed motor vehicle insurance prices rose 11.3 percent in 2024, following an even larger 20.3 percent increase in 2023. (bls.gov)

That broader backdrop matters because tariffs do not hit the market in isolation. They land on top of a system where insurers are already dealing with high-cost claims and more expensive repairs. CCC Intelligent Solutions notes that tariffs and supply-chain disruption are amplifying cost pressures throughout automotive manufacturing, repair, and insurance economics. (cccis.com)

What Tariffs Mean for the Auto Industry

A tariff is essentially a tax on imported goods. In the auto sector, tariffs can apply to fully built vehicles, key components, raw materials, or subassemblies that flow through global supply chains before a car is sold or repaired.

In March 2025, the White House announced a 25 percent tariff on imported passenger vehicles and light trucks, as well as key automobile parts including engines, transmissions, powertrain parts, and electrical components. The administration later stated that tariffs on automobiles took effect on April 3, 2025, while tariffs on automobile parts were set to begin on or after May 3, 2025, subject to related implementation details. (whitehouse.gov)

Even where exemptions or content-based adjustments apply, tariffs can still raise costs, complicate sourcing, and force manufacturers and suppliers to rethink production and logistics. (whitehouse.gov)

How Tariffs Can Raise Car Insurance Premiums

Insurance premiums are based in part on what insurers expect to pay when claims happen. Tariffs affect that math in several important ways.

1. Higher Parts Prices Mean More Expensive Repairs

Modern vehicles rely on a large number of imported or globally sourced parts. If tariffs raise the cost of those components, repair shops pay more, insurers reimburse more, and claim severity rises.

This is especially important for newer vehicles packed with sensors, cameras, driver-assistance systems, specialized lighting, and electronic modules. A repair that once involved replacing a simple part may now require calibration, programming, and brand-specific components.

When claims cost more to settle, insurers usually respond by raising premiums over time.

2. Higher Vehicle Prices Raise Total-Loss Payouts

Tariffs do not affect repairs alone. They can also increase the price of new vehicles and, in some cases, support higher replacement values across the market.

If a vehicle is declared a total loss after an accident, the insurer must pay based on the car’s actual cash value or replacement-related valuation under the policy terms. When vehicle prices rise, total-loss settlements become more expensive.

That higher payout exposure can put upward pressure on premiums, especially for full-coverage policies.

3. Supply Chain Disruptions Can Extend Repair Times

Tariffs can do more than raise sticker prices. They can also push manufacturers and suppliers to switch sourcing strategies, reroute shipments, or absorb delays while new trade and compliance processes take effect.

CCC reports that tariffs are helping redraw supply chains and creating a more expensive, less predictable operating environment across the auto ecosystem. (cccis.com)

Longer repair times create downstream insurance costs such as:

- Extended rental car coverage

- Longer storage periods

- Delayed claims resolution

- More pressure on repair networks and parts availability

Those extra claim-handling costs can also flow back into premiums.

4. More Vehicles May Be Declared Total Losses

When repair costs rise sharply, insurers may decide that fixing a damaged vehicle no longer makes economic sense. In those situations, more vehicles may cross the threshold from repairable to total loss.

That creates two consumer impacts at once:

- The insurer may face a larger settlement payout

- The driver may need to replace the vehicle sooner, often in a higher-cost market

Both outcomes reinforce the same trend: rising insurance costs tied to rising automotive costs.

5. Theft Risk Can Become More Expensive to Insure

When vehicles and replacement parts become more valuable, theft-related claims can become more costly too. Higher-value components create stronger incentives for organized theft, parts stripping, and fraud.

Insurers do not price theft risk based only on tariffs, but anything that raises the value of vehicles and repair parts can increase the cost of comprehensive claims.

Why This Hits Some Drivers Harder Than Others

Tariff-related cost pressures will not affect every driver equally.

Premium increases can vary based on:

- The make and model you drive

- How expensive the parts are for your vehicle

- Whether your car uses advanced driver-assistance technology

- Whether your insurer writes a lot of business in high-loss states

- Your location and local repair costs

- Whether you carry full coverage or liability only

Drivers of newer imported vehicles, luxury vehicles, EVs, and vehicles with expensive sensors or specialized components may feel the impact more quickly if repair or replacement costs rise.

What Drivers Can Do to Manage Rising Insurance Costs

You cannot control tariff policy, but you can take steps to reduce your insurance exposure.

Shop Rates More Often

Rate differences between insurers can be significant, especially after broad market repricing. If your renewal jumps, compare quotes before accepting it.

Review Your Deductible Carefully

A higher deductible can reduce your premium, but only choose one you could realistically afford after a claim.

Check Discounts You May Be Missing

Many insurers offer discounts for bundling, safe driving, telematics participation, anti-theft devices, low annual mileage, or paperless billing.

Research Insurance Costs Before Buying a Vehicle

A car’s insurance cost can vary widely based on repair complexity, theft risk, safety record, and replacement value. It is wise to estimate insurance before you buy, not after.

Consider Repair-Cost Risk Alongside Purchase Price

A vehicle that looks affordable upfront may be much more expensive to insure and repair over time. That is especially true for models with expensive body panels, imported parts, or complex electronics.

Why This Matters for Used-Car Buyers Too

Tariff-related insurance pressure is not only a new-car issue. Used-car buyers can feel the effect as well.

If repair costs rise, insurers may increase rates for older vehicles too, especially when replacement parts, used parts, or repair labor become more expensive. In some cases, higher repair costs can also reduce the threshold for totaling an older vehicle after a moderate crash.

That means used-car shoppers should think beyond purchase price and factor in long-term ownership costs such as premiums, repair risk, and parts availability.

Final Thoughts

Tariffs can raise car insurance costs because they increase the price of repairing and replacing vehicles. Once parts, materials, or imported vehicles become more expensive, insurers face higher claim costs. Over time, those higher claim costs are often reflected in the premiums drivers pay.

This does not mean every policy will spike overnight or by the same amount. But it does mean tariffs can contribute to a broader pattern of rising auto ownership costs, especially when the market is already dealing with elevated repair complexity and inflation-driven claim severity.

For drivers, the smartest response is practical: compare insurance options regularly, understand how your vehicle affects premium risk, and factor insurance into every vehicle purchase decision rather than treating it as an afterthought.

If you are shopping for a vehicle, it is also worth checking broader ownership and risk data before you buy. Researching repair trends, market value, and vehicle history can help you avoid a car that costs more to own than expected.

Author

Nathan Whitmore

Nathan Whitmore is an automotive research writer focused on vehicle history reports, VIN analysis, title verification, and used-car background checks. He writes practical, consumer-friendly content that helps buyers understand how ownership records, accident history, branded titles, and lien data can affect a vehicle’s value and legal standing. His work is designed to make complex vehicle records easier to interpret before a sale is finalized.